How will the COVID Pandemic Affect Health Insurer and Provider Quality Rating Scores?

by Richard HamerOverview. The pandemic caused a great downturn in health care utilization and a great migration of services to online platforms. What this has done to enduring relationships providers and health plans have with their customers will be seen in upcoming CAHPS scores. However, those surveys won’t measure the impact of specific consumer experiences on their health system quality ratings. A quality rating diagnostic survey can be specially crafted to assure CAHPS/QRS results can be acted upon.

Across the Economy reports are showing that the pandemic disrupted relationships between people and businesses. Prominent examples come from many industries including retail, hotels, airlines, online retailers, and health organizations.

The disruptions can be found in several different instances. For retailers, the failure of staff to mask-up and social distance led customers to question their competency. For hotels a below-expectations pandemic response was correlated to lower customer satisfaction ratings recorded after the stay. For airlines, sensitivity to and acknowledgment of passenger experiences and perceptions was a key to preserving loyalty and satisfaction. And for online retailers, low satisfaction is related to poor website performance, lack of inventory, unresponsive customer support, and missed shipping expectations.

The pandemic changed the relationships between people and the organizations they deal with, including both health providers and insurers. How those relationships changed has yet to be fully illuminated.

Key Unknowns. An unknown that continues to reverberate through the health system is the impact on relationships created by the great 2020 downturn in health services utilization. To provide a sense of scope, we turn to the American Hospital Association report on financial performance during the four months of March through June 2020. AHA says that cancelled surgeries, outpatient treatment, and other services caused hospital revenues to drop, on average, $50 billion in each month. For insurers the downturn means a lack of member interaction affecting insurers just as lack of patient interaction has affected providers. Key questions have answers that can be gained through survey research:

- During the pandemic, did insurers or providers contact consumers to re-schedule appointments, offer telemedicine alternatives, and otherwise check in? If they did or they didn’t, what did this do to consumer overall loyalty and satisfaction? How will this impact be seen in the upcoming results of CAHPS surveys?

- Were health organizations flexible and thoughtful about their communications? Did they use preferred channels (text, call, email, etc)? Did they use the right volume of communications?

- How many consumers were triggered by the lapse in medical services to find a new doctor? What did that do to their relationship with their insurer?

Not interacting as much means fewer opportunities to satisfy patients or members.

A second unknown for both providers and insurers is the impact of telehealth on people’s loyalty and satisfaction. Everybody knows the pandemic led to more telehealth usage. But the aftermath of this large-scale shift in health care delivery is still being discovered.

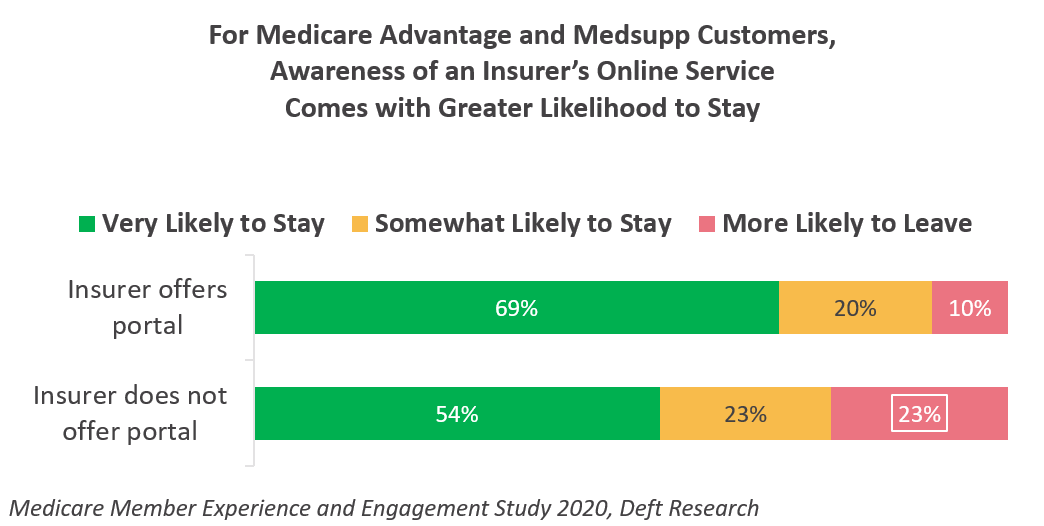

From our research, we know that access to digital tools and platforms is associated with greater loyalty of health plan members. The graph to the left provides some of that evidence: for Medicare Advantage and Medsupp customers, awareness of an insurer’s online portal is associated with a greater likelihood that members will stay with their insurer.

From our research, we know that access to digital tools and platforms is associated with greater loyalty of health plan members. The graph to the left provides some of that evidence: for Medicare Advantage and Medsupp customers, awareness of an insurer’s online portal is associated with a greater likelihood that members will stay with their insurer.

If they are to manage quality ratings and member experiences, the digital factor is something insurers and providers have not yet measured as thoroughly as they might. If the ways digital services were linked to overall health plan/health provider rating and CAHPS scoring were fleshed out, organizations would have important input into their ongoing digital investment. This would give them the opportunity to use the predicted impact on quality rating scores as one input in investment decisions.

Digital services, including telemedicine impact the member and patient experience in several ways:

- During the pandemic, the copayments for telemedicine were waived or reduced by many organizations. As we have shown, the cost sharing differential has an impact on whether people will choose telemedicine over a traditional office visit. Now, with the pandemic subsiding, will consumer loyalty and satisfaction be compromised if telemedicine costs are increased? How much did the previous cost sharing policy contribute to or detract from this year’s quality rating scores?

- Telemedicine and other digital services are potential time savers, and many consumers prize convenience over all else. Through research, health organizations have the opportunity to actually measure the importance of convenience and time savings provided by their online systems. From this they can make more informed decisions about the features to provide and the policies governing their use and cost.

- Online systems can offer easier access to a menu of physicians and their availability. For health organizations, management of such tools can be improved with knowledge of their impact on coordination of care and other health system outcomes as well as the impact on different populations — aged persons for instance.

- Ancillary online services also play a role in consumer satisfaction. For example, prescription ordering and refills are commonly available on online systems, but their contribution to consumer loyalty and satisfaction is not always known. Help navigating to physical therapists and other providers may or may not have a strong impact on quality ratings.

- For many specialist visits, online services and telemedicine are less preferred. Urology, eye/ear/nose/and throat visits, pulmonary medicine, dermatology, all benefit from or require an in-person visit. As the use of digital tools continues to grow, health organizations will want to make sure consumer engagement and loyalty is not harmed by the platform getting in between doctors and patients.

Conclusion. This year, evaluation of quality ratings will have a new wrinkle — the pandemic’s disruption of consumer relationships with providers and health insurers. The disruption will essentially add variability to people’s experiences and perceptions, and so CAHPS and QRS results may be less predictable and less understandable. Diagnostic surveys can be conducted ahead of the official rating surveys to test the hypotheses above and others.

Find out more — filling the form below will let our research experts know you’d like to discuss this topic.